Introduction

Money doesn’t shout; it presses quietly

“The biggest mistake investors make is focusing on returns instead of focusing on risk.”

— Howard Marks, The Most Important Thing

Howard Marks was talking about investing in the above quote, but the same mistake can appear long before anyone ever buys a stock. It shows up quietly in everyday life.

A knock at the door. A phone call that was never made. A couple having a conversation late at night, when their children were supposed to be asleep. None of these feels like a financial decision, but each of them is. People are not reckless or irresponsible. Still, something feels heavy in these moments. That weight is fragility.

I have seen capable, disciplined people live with constant financial pressure, not because they lacked ambition, but because they were building progress without structure.

They focused on growing income but not protecting it. They made good decisions, but those decisions were not well connected to each other.

That imbalance created a specific kind of stress—not panic, not chaos, but something quieter and more exhausting: the sense that one mistake could undo everything.

Money felt heavy long before I understood why. I grew up in a family where money was uncertain. Years later, working in investing, I saw the same pressure at every income level. I now work as a hedge fund CFO, where I’ve seen these patterns play out repeatedly across individuals, families, and institutions. Different numbers, same underlying pressure. That’s when I realized the problem wasn’t income. It was structure. That insight became the foundation for everything in this book.

My family worked relentlessly and still never felt secure. Our small businesses would first show promise, but then fade. When opportunities disappeared, my parents left to find work elsewhere. Responsibility arrived early in my life. Clarity came much later.

In that environment, I formed a belief: if life was going to change, it would start with me. That belief pushed me toward education and opportunity. It also came with debt, which my family carried so I could have those chances. I felt that weight every day.

As my career advanced, the outside story looked clean. Inside, things still felt fragile. Every incoming dollar had a job to do. Every decision carried pressure. I repaid my debt, supported my family, and spent carefully; but even as my income rose, I still felt a sense of urgency.

For years, I focused almost entirely on money. Earn more. Save later. Fix everything after the next milestone. Then, slowly, something shifted.

I began saving and investing consistently. The amounts were modest, and the progress didn’t feel remarkable, but it was steady. My anxiety softened. Decisions became easier. The sense of pressure began to lift.

I was not wealthy, but I was no longer fragile.

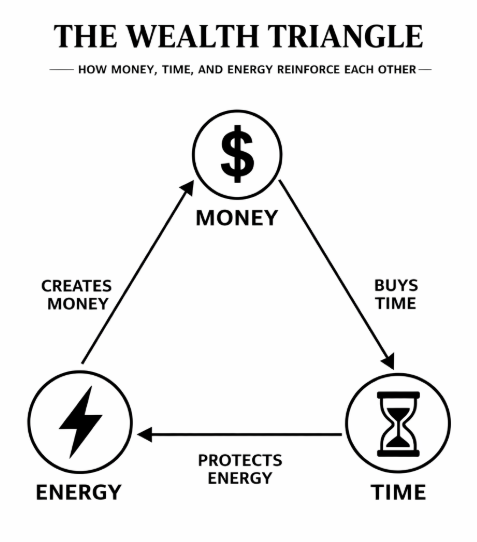

That was when I understood what most financial advice misses. Wealth is not built on money alone. It is built across three resources: money, time, and energy. Money is measurable. It is tracked and optimized. Time is limited. Once spent, it cannot be recovered. Energy is your capacity to focus, decide, and act consistently.

As the illustration shows, when money, time, and energy work together, financial and emotional stability compound.

Wealth is often measured only in money, but I don’t think money alone creates a good life. It provides security and options, but time determines how freely you can live, while energy determines how fully you can engage with life and the people around you. When any one of these resources is depleted, the others lose their value.

Most people try to improve one of these aspects while unknowingly draining the other two. They earn more money, but lose time and energy. They pursue better returns, but increase complexity and stress. They optimize efficiency, but burn out in the process. Each decision may make sense on its own; but without a system, the pieces don’t work together.

This is why progress feels slow, fragile, or unsustainable. This book offers a different approach. It presents a proven system for building wealth across money, time, and energy. They are separate concepts, but they work together here as interconnected parts of a structure that compound over time.

This book is not a rewrite of old wisdom. I attempt in this book to translate these timeless principles into modern life, grounding them in how people think, feel, and decide here in the 21st century. They are organized around a structure I call the Seven Pillars of Wealth, a set of practical foundations that strengthen your financial life step by step. They are not tricks or shortcuts, but powerful bases upon which to build.

Each pillar is simple on its own, but together they form a system designed to create financial security without sacrificing time; reduce stress by simplifying decisions; and build progress that is steady and durable.

The pillars are built on each other in sequence. We begin by creating margin to build a financial and emotional cushion. We learn to direct that margin intentionally by prioritizing what we spend it on. We then allow time to compound it. We protect what we have built. We position our housing choices wisely to support it. We then prepare for uncertainty while expanding our earning power.

The chart above was designed to emphasize that small, consistent actions reinforce one another. As the cycle repeats, stability increases, fragility declines, and wealth compounds.

The ideas in this book aren’t new or complicated. They are simple and proven. That is exactly why they work.

Knowing them, however, is one thing; organizing them into a structure that holds up in real life is another.

As my career has evolved, I have seen this clearly in another context, that of financial markets. There, the difference between success and failure is rarely between smart and foolish people; it is between systems that absorb stress and systems that break under it. The same is true in personal finance.

Our money decisions are never purely logical. They are shaped by emotions such as fear, urgency, guilt, pride, and confidence. When we ignore this emotional layer, we fail in practice, even if we follow good theoretical advice. When money, time, and energy are aligned, something different happens. Our financial stability improves. Our emotional pressure declines. Our progress begins to compound.

Think of this book as a set of frameworks, not prescriptions. Your situation will be different, and your path should reflect that.

If money has ever felt heavy in your hands, if progress has felt slower than it should be, or if you have done everything right and still feel uncertain, rest assured that you are not broken. You are simply missing a system. The Seven Pillars of Wealth provides that structure.

Each pillar builds on the last. Together, they reduce fragility, increase stability, and allow wealth to grow in a way that holds up over time.

The goal is not just to grow money, but to protect the time and energy that make wealth worth having. Now, let’s begin.

Reader Resources

To help you apply the ideas in this book, I have created a collection of companion resources and worksheets, available online for free at:

Chapter 1: Pay Yourself First

Keeping the first slice to earn self-respect

“Wealth is what you don’t see.”

— Morgan Housel, The Psychology of Money

Most people assume wealth is always visible. They think of large houses, expensive cars, and other obvious signs of success. The opposite, however, is usually true. The wealth that truly changes lives is often the wealth no one sees.

Earlier this century, a man named Geoffrey Holt lived quietly in a mobile home park in Hinsdale, New Hampshire. He worked as a groundskeeper there, mowing lawns and maintaining the overall property. He wore simple clothes, drove an old vehicle, and kept largely to himself. To most people in town, he looked like someone who was only just getting by.

When he passed away in 2023, however, the town discovered something unexpected. He had quietly accumulated $3.8 million, which he left to the community to support education, recreation, and local services.

How does someone earning an ordinary income build that kind of wealth?

Most people assume wealth comes from high salaries, successful businesses, or lucky investment windfalls.

Geoffrey Holt had none of those advantages. What he had was something far simpler. For decades, he followed a quiet rule most people ignore: keep the first slice. When receiving a small but decent settlement after the closure of a grain mill where he was a manager, he invested it instead of upgrading his lifestyle. That small decision, repeated year after year with each annual dividend, created the kind of invisible wealth that most people never see.

In both my own life and later professional work, I’ve learned that the difficulty in building wealth is rarely mathematical. The numbers are usually clear. I find the real obstacle is emotional friction. Fear, pressure, and urgency distort decisions long before spreadsheets do.

This chapter is about that first principle, that building wealth is not about high income or clever investing. The foundation is simpler: keep part of what you earn and do so before optimizing your finances.

Financial wealth begins as emotional wealth. It starts with restraint and with margin built intentionally into the system.

Most people struggle not because they earn too little, but because their financial lives lack margin—the amount of money they have above the amount they need to pay their bills.

Paying yourself first is not just a savings tactic; it’s a structural rule that changes how money behaves in your life. It creates stability before growth, and protection before progress.

It isn’t just about money, but also about creating margin across three resources. It creates margin in money, which builds security. It creates margin in time, which creates flexibility. In addition, it creates margin in energy, which reduces pressure.

That margin is where everything else begins. This chapter will show you how to build that margin, one paycheck at a time.

The First Time I Paid Myself First

Long before I understood compound interest or retirement accounts, I learned this principle in a different way.

When school tuition came due the year I was nine, money was tight; my parents were away working, and my grandparents were doing their best to care for us. That week, I took out a small metal box where I would keep my allowance and holiday money when it came in. It wasn’t much, but it was the first money I ever personally controlled.

I used it to pay my tuition, so my education wouldn’t become a burden to my grandparents. I didn’t realize it would happen, but something shifted in my mind that day.

I inherently understood, without needing it explained, a principle that would shape my life for years to come: the money I keep for emergencies shapes me more than the money I spend on frivolous things.

That’s why I start with the concept of paying yourself first in the Seven Pillars framework. Keeping the first slice of what you earn changes your relationship with money. It helps you build self-respect, create margin, and separate who you are from any chaos that might be happening around you.

We all have a moment—early or late—when we realize that wealth does not begin with income. It begins the first time we set aside something for the future and decide it belongs there. For me, that moment came from a metal box at the age of nine; for you, it can begin with your very next paycheck.

The Rule of 10 Percent

Years later, I found myself in a small Brooklyn apartment. It was 2012. I had just paid rent. My bank balance was low, and I was doing the familiar math: groceries or buffer? I remember the realization clearly: if I kept living on the edge, life would keep pushing me over it.

What I organically learned as a child through necessity, I later had to relearn as an adult through deliberate structure. That night, for the first time, I drew a line between who I was and who I wanted to become.

I created a new rule for myself: 10 percent of every paycheck goes to a Future Me savings account, automated so that I didn’t even have to think about it.

I didn’t wait until I “felt ready,” and I didn’t make exceptions when things got tight. I didn’t realize it then, but I wasn’t just changing my budget; I was redesigning how my entire personal financial system worked.

When the first transfer happened, I didn’t feel richer, but something important had shifted.

I had created margin—small but real—a buffer I had never had in my life before. That single act didn’t transform my life overnight, but it did change the direction of my life immediately.

For the very first time, my savings began to grow, and my anxiety began to ease. The question that used to follow every purchase— “What if?”—no longer ran the room. I was not just surviving anymore; I was preparing.

Every automated transfer sent the same message: I matter, my future matters, and I am willing to prove it. This is why the Rule of 10 Percent works.

What I began as a financial habit started to change something else for me. I was not only building savings, but also creating space in my time and stability in my energy.

Note that this rule is not about the amount, but rather about the identity it builds. Ten percent is not a magic number; that is a starting signal.

We can’t negotiate with the principle, but we can adjust the percentage based on our circumstances. No matter what that amount is, when you keep the first slice of every dollar, you stop treating your future as an afterthought and instead start preparing for it.

The more you follow this rule, the more you get used to it, and the more solid the foundation you lay for the subsequent pillars.

Preserving Capital Before Consumption

Another winter night in New York, I got off at the wrong subway station. I checked my transit card balance and realized I could not swipe back in without risking an overdraft. So, I zipped up my jacket and walked the distance instead.

That wasn’t a dramatic decision—it was only a 15-minute walk—but when you are close to empty, small choices carry a weight far beyond the literal number. That walk clarified something important to me: wealth is not about how much you earn, but whether you keep any of it.

For a long time, I lived in what I now recognize as consumption mode. Money came in and went right back out—not recklessly, but certainly without thinking about it. I had a purpose for every dollar, but none of them belonged to the future.

What I eventually realized is that wealth begins the moment you exit consumption mode and enter preservation mode. That shift requires discipline, not abundance.

It starts with a simple rule: no matter how many or how few eggs in your basket, keep one. It’s that act that changes how you relate to money, not how many eggs you have in total.

When you decide that one portion of what you earn is untouchable, you stop treating money as something life takes from you. You start treating it as something you protect. That shift matters more than the amount.

Most people consume everything they earn and tell themselves they will save later—when their income rises, when their life calms down, when they can “finally afford it.”

But wealth starts when behavior changes, not when conditions improve. In fact, the higher your income, the more expensive it becomes to delay this habit. Your lifestyle expands faster than your discipline if you don’t protect your savings.

Keeping one egg is how you prove to yourself that the future exists and matters. This principle scales; whether you earn $500 a week or $5,000, the habit is the same. Over time, that preserved portion becomes momentum. The momentum helps you gain more confidence. As your confidence increases, you also expand your capacity.

Delay Is an Invisible Tax

Most costly decisions don’t feel costly at the time. They feel small, reasonable, and easy to postpone.

When people imagine financial setbacks, they picture dramatic events, such as job losses, medical bills, and market crashes.

The most common obstacle, however, is not a crisis but a delay. Not because people are irresponsible. Not because they don’t understand money. But because they delay the moment when saving becomes non-negotiable. Income does not fix this problem. Structure and margin do.

Early in my career, I told myself I would start saving and investing later—when my salary was higher, when life felt calmer, or when there was more breathing room. That logic felt sensible, but it was flawed. Time, not income, does most of the work of building wealth. The real cost of waiting is not missed dollars but missed years.

Compounding rewards those who start before they feel ready. Early contributions buy time. When saving is delayed, no amount of effort later can fully replace that lost time.

This is why two people with similar incomes and investment strategies can end up in very different places. The one with more wealth didn’t make better decisions, but simply made them earlier.

That is why paying yourself first matters so much. It removes the option to delay and turns intention into action before doubt has time to intervene. You stop hoping the next raise will change things. You stop waiting for perfect conditions. Wealth begins the day that waiting ends, and when saving becomes automatic and future focused.

The Emotional Wealth Hidden in Saving

Most people think saving is about numbers. But its most powerful effect appears long before the numbers grow.

Saving changes how money feels. When you begin keeping the first slice of what you earn, something subtle shifts. The constant background tension eases. Decisions feel lighter. You aren’t rich, but you are no longer fragile.

Before I saved consistently, money felt loud. Even small purchases carried weight. There was no margin to absorb mistakes. When something is set aside for the future, you stop holding your breath. Urgency fades. Panic softens. This is the return most people underestimate.

Saving doesn’t create excitement. It creates safety. Not from growth, but from margin. Margin isn’t comfort; it is decision quality under pressure. When margin exists, mistakes are survivable. Choices widen. Time begins to work in your favor.

What you are really building is not just a bank account balance. You are building distance from pressure, which gives you the ability to wait, the ability to choose, and the ability to say no without fear. That is where emotional wealth begins.

Common Frictions

Barrier 1: “I have debt. Shouldn’t I pay that off first?”

This is one of the most common concerns about paying yourself first, and a reasonable one.

Paying yourself first does not mean ignoring debt. It means refusing to leave your future completely unprotected while you address the past.

Even while paying down loans, setting aside a small, consistent amount builds margin, and prevents one setback from forcing you deeper into debt. A modest emergency fund prevents the shocks of taking on new high-interest debt. The principle is not the percentage. The principle is continuity.

Barrier 2: “I have nothing left over to save once I pay my bills.”

When money feels tight, saving can feel unrealistic. But this is often when saving matters most.

Paying yourself first does not require large amounts. It requires a line in the sand; that no matter how small it is, something gets set aside before spending absorbs everything.

Even small, automatic transfers create proof that the future exists and deserves a claim. Over time, that proof changes behavior.

Barrier 3: “I’ll start once my income is higher.”

Paying yourself first is rarely a timing issue. It is usually a structural one. When income rises before savings habits are set, your spending simply expands faster. Starting to save earlier, even at a small scale, anchors the behavior before “lifestyle creep” has a chance to consume it.

The habit matters more than the amount. Wealth begins the moment you keep the first slice.

Chapter 1 Summary

- Wealth begins with a decision, not a number. Paying yourself first is the moment you claim your future before life consumes the present.

- Financial stress is rarely caused by low income. It is usually caused by living without margin. Having extra money for emergencies reduces urgency, restores choice, and changes how decisions are made under pressure.

- Waiting feels harmless, but it is actually expensive. Time rewards those who build structures early, not those who wait for perfect conditions. Starting small, even before you feel ready, is the advantage. The habit matters more than the percentage. Keeping the first slice anchors behavior before income, lifestyle, or excuses can erase it.

- Emotional wealth arrives before monetary wealth. Calm, stability, and resilience make long-term wealth possible.

- This pillar strengthens money by building financial margin, expands time by creating future flexibility, and preserves energy by reducing financial pressure.

Chapter 1 Action Plan

- Automate the first slice. Automatically route money into savings before becoming tempted to spend it. Start at 10 percent if possible. If not, start smaller—but make it automatic and untouchable.

- Separate it physically. Move this money to a different bank account and name it with intent (e.g., Future Me). What’s separated survives.

- Create margin on purpose. Remove or downgrade one lifestyle expense this month, so saving doesn’t feel like deprivation.

- Observe, do not manage. Once a week, quickly look at the Future Me balance to see the current total. No changes. No judgment. Just awareness.

- Do it now. Within 24 hours of reading this chapter, complete one concrete action—set up the payroll automation, put an amount of money into savings, or skip one lifestyle expense. Momentum starts with evidence.

Paying yourself first does not solve your money problems. It reveals them. It also changes how you use your time and how you experience your energy.

Once the first slice is protected, every remaining dollar demands intention as well. The next chapter is about this intention—choosing what truly supports your life, then letting go of the rest without guilt. guilt.

*************************************************************************

Enjoy reading so far. Please check out the book on Amazon. I look forward to hearing your thoughts on what resonates.

*************************************************************************